Jonathan Portes delves into the data on the economic performance of the UK after its exit from the EU’s single market and customs union on 1 January and assesses the real-world impact of these new trade barriers

The economics profession came in for opprobrium and derision after the 2016 EU Referendum, when the recession predicted by the Treasury and the International Monetary Fund failed to materialise.

While not all economists share the blame for then Chancellor George Osborne’s scaremongering, it is fair to say that at least some of the criticism was justified.

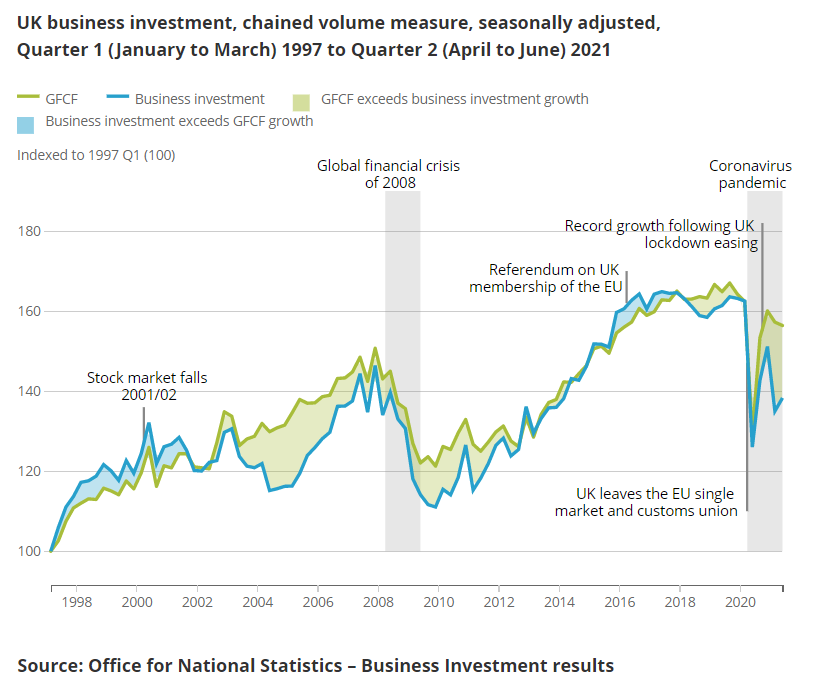

Before the Coronavirus pandemic, the UK’s economic performance was mediocre – worsened in part by the vote to leave the EU, as uncertainty hit the pound, and reduced investment, which stagnated after the referendum. But it was not disastrous, as most businesses simply opted to wait to see what would happen, rather than rushing for the exit.

But, somewhat paradoxically, analysing the impact of economic changes is easier over the long than the short-term – it is easier to forecast the climate than the weather.

Forecasting the short-term impact of the Brexit vote was, by definition, about assessing the impact of a political shock on essentially psychological variables – consumer and business confidence, and expectations about future policy. Neither economics nor anyone else has a great track record on this. In retrospect, the fact that predictions were way off should not have been a great surprise.

But, over the longer term, Brexit is primarily about changes to the trading relationship between the UK and the EU. And here, economics and economists, can do better. There are a lot of issues in economics that are controversial, but the principle that increasing trade barriers between two trading partners will reduce trade, and that in general that will reduce economic welfare on both sides, really isn’t.

While putting precise numbers on those impacts is hard, and requires complex economic modelling, it really would be surprising – and a genuine challenge to conventional economics – if Brexit didn’t do some damage to the UK economy. While there was no shortage of politicians who argued that somehow new trade barriers would not make much difference, or that trade with our closest and largest single trading partner could easily be substituted with trade with the rest of the world, no credible economic analysis endorsed such claims.

So, with six months of data on the economic performance of the UK after its exit from the EU single market and customs union on 1 January, what can we say about the real-world impact of these new trade barriers?

Trade

The initial impacts were very much as trade experts – and common sense – would have predicted: trade with the EU, especially imports, rose sharply immediately before the turn of the year, as businesses stockpiled goods in anticipation of Brexit-related disruption; then fell even more sharply, before slowly recovering.

Most of these transitional impacts should have worked through by now. Perhaps surprisingly, UK exports of goods to the EU have now recovered roughly to their pre-Coronavirus levels. But imports from the EU are down substantially, by about 10% compared to two years ago, partly offset by an increase in imports from the rest of the world.

The most surprising – and arguably worrying – statistics relate to the UK’s exports to the rest of the world. Far from Brexit providing a boost, these are also down by about 10%. And this is not an effect of the Coronavirus – EU exports to the rest of the world have increased, not decreased.

Overall, therefore, the UK’s trade performance has been extremely weak.

How much of this is due to Brexit is unclear. The data is noisy and unreliable and will almost certainly be revised. And we know even less about services trade, which makes up about 40% of UK exports to the EU, although a much smaller share of imports.

There hasn’t been much disruption to financial services, but that doesn’t mean that Brexit doesn’t matter. Firms knew that it was coming, and the picture remains a slow and gradual transfer of some business to continental Europe. In other business services – including law, accountancy, and creative sectors – trade is more dependent on the physical movement of persons, meaning that the impact may be larger but has so far been obscured by Coronavirus-related restrictions.

Perhaps more importantly, it is still very early days. The models described above look at effects over the long-term – say 10 or 15 years – rather than six months. Over time, as companies restructure their supply chains or decide where to invest, the impact is likely to grow. But, so far at least, there is no reason for economists to change their minds about Brexit and trade.

Wages

On wages, the economic consensus was reasonably clear. Just as new trade barriers reduce trade and make us somewhat worse-off, so do barriers to the movement of people. So ending free movement will hit growth. But migration, like trade, also has distributional impacts – workers who compete with migrants might in theory benefit from reductions in immigration.

However, the evidence also suggested that any such impacts would be small. A study by Bank of England economists (often cited by anti-immigration activists) found that wages in the most affected sectors might have been pushed down by about 1% over a decade of high immigration – an impact the study’s authors described as “infinitesimal”, compared to the other drivers of pay.

More importantly, simply looking at the direct impact misses the point. If lower immigration reduces overall growth and productivity, and hence tax revenues, then the average worker will certainly lose out, and even those workers who gain directly can end up losing indirectly. My own pre-Brexit analysis suggested that these indirect effects would indeed dominate.

So do reports of staff shortages and – so far largely anecdotal – higher wages in those sectors where migrants make up a large share of the labour force somehow prove us wrong and show that the end of free movement is indeed a boon for workers?

Hardly. The past 18 months have seen huge shocks to the UK labour market. First, the forced closure of large sectors of the economy, leading to the furlough or letting-go of millions of workers – many of whom were from the EU and quite understandably decided to return to their home countries, temporarily or permanently; and then the reopening of those sectors, while huge uncertainty remained, as well as stringent travel restrictions in both directions. It would frankly have been astonishing if this hadn’t resulted in major disruption to both the supply and demand of workers in the affected sectors, and hence labour shortages.

This has little do with Brexit, at least directly, with the possible exception of agriculture and the transport sector – although here other factors are also at work. It was the pandemic that caused the exodus and most of those who left will, despite Brexit and the end of free movement, have the right to return here should they so wish under the settled status scheme.

More importantly, it tells us little about the medium to long-term impacts on wages, direct or indirect, of the end of free movement. For precisely the same reasons, Brexit opponents should not overdo the doom and gloom about empty shelves or food shortages: these are by no means all down to Brexit, and in any case are likely to be transitory.

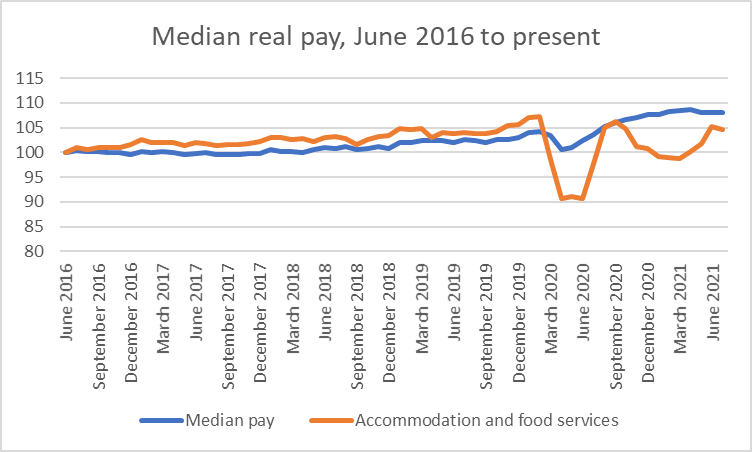

Indeed, if we look at the actual data, rather than anecdote, we don’t see much to suggest a wage explosion. It is possible that anti-immigration nativists such as Paul Embery – who claimed in 2018 that wages in hospitality were soaring (they weren’t) and that this showed the malign impacts of migration (it didn’t) – will be right this time. But claims that wages are soaring aren’t supported by hard data yet. Despite the recovery, real wages in the accommodation and food services sector are still below their pre-pandemic levels.

Inflation

The most obvious impact of shortages and bottlenecks, in the labour market and elsewhere, is on inflation, with prices up more than 1.5% just in the last three months, and some disruption to retailers’ supply chains.

This is, of course, a cost to all workers (and the rest of the population), including the lowest paid, and directly reduces real incomes. So even if there has been some upward pressure on wages in cash terms, it’s far from obvious, as yet, that the net impact on living standards is positive. As with trade, there isn’t, as yet any obvious reason for economists to change their minds.

And what about the other benefits of Brexit – trade deals with third countries, deregulation, and so on? Here we can be pretty definitive – nothing that has happened so far amounts to more than a rounding error; nor is there any reason to believe that, in the short-term at least, this is likely to change.

It is possible that the UK will diverge radically from the economic model of the past four decades, with big impacts – positive or negative – on UK economic performance. But, as Anand Menon and I pointed out, if anything, both the pandemic and Brexit seem to have made the UK more, not less, European.

So all sides are likely to be disappointed. Barring unforeseen events, Brexit will not lead to a crisis nor precipitous economic decline; but the economic downsides remain more tangible and durable than any likely benefits. As I wrote just before the changes took effect, a slow puncture not a car crash.