Read our Monthly Magazine

And support our mission to provide fearless stories about and outside the media system

As the Iran war and the Strait of Hormuz crisis have driven fresh panic about energy security, a familiar set of voices has moved quickly to turn that fear into a renewed case for more North Sea drilling. But the institutions leading the charge have deep financial and institutional ties to the fossil fuel industry.

A Byline Times investigation reveals how the rest of the press has largely failed to reveal these conflicts of interest – despite the claims being contradicted by official data from the North Sea oil industry.

The Lobby

On the Telegraph’s Planet Normal podcast, Andy Critchlow argued that Britain’s retreat from the North Sea amounted to “economic self-harm”. Critchlow was described as an ‘energy supply expert’, but he is actually head of news at S&P Global, the oil-and-gas pricing and conference business that runs CERAWeek – Big Oil’s global energy summit – and which provides data to the Secretariat for OPEC, the consortium of massive oil producers dominated by the Gulf regimes.

S&P Global’s vice chairman Daniel Yergin, who chairs CERAWeek, has for years advanced an “energy addition” thesis – the view that renewables are being layered on top of fossil fuels rather than displacing them.

A similar line was pushed weeks before the war by the Tony Blair Institute, which declared that allowing UK oil and gas production to fall faster than demand would increase Britain’s exposure to international markets and geopolitical risk.

The new report drove big headlines in Bloomberg, Politico, Telegraph, The Times and Financial Times. However, they mostly failed to inform their readers that TBI has received funding from Gulf oil producers, chiefly the Saudi Government, and advised the UAE Government, or that Blair has personally consulted for Gulf petrostate interests and spent much of his time as prime minister promoting British Petroleum (BP).

The same pattern holds at the Tufton Street based Institute of Economic Affairs, which in a February 2026 paper announced that meeting Britain’s oil and gas needs through imports would be more environmentally harmful than domestic production, and called for repeal of the Energy Profits Levy and continued development of North Sea resources.

The same IEA received more than £640,000 from fossil fuel companies and Rupert Murdoch’s media empire between 1957 and 2005, including substantial funding from BP, Shell and Esso; and has been funded by BP every year from 1967 to 2018. Yet that tidbit was excluded in the amplification the IEA paper received from the Telegraph, Daily Express, GB News, and The Critic.

Trump’s Iran War Threatens a Refugee Crisis on a Scale That Dwarfs Syria

A former senior US defence analyst warns that the assault on Iran risks causing a refugee crisis up to four times larger than what happened during the Syria conflict

What the Official Data Actually Shows

Even where media coverage did cite some criticisms of these claims, it largely failed to lay bare the fundamental data sleights-of-hand at play.

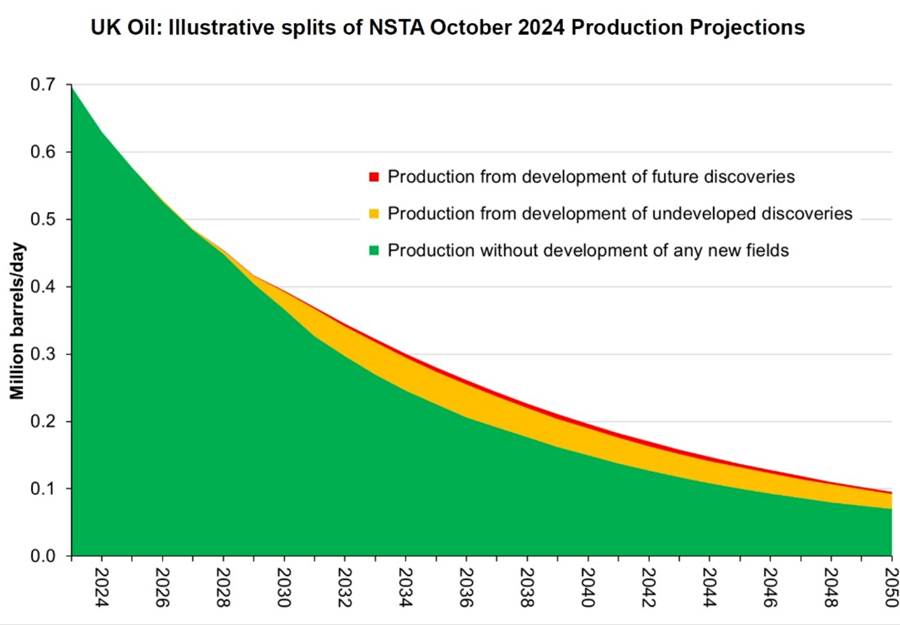

Proponents of new drilling frequently cite “20 billion barrels” remaining under the North Sea. That figure collapses different categories into one politically convenient soundbite. In reality, the North Sea Transition Authority puts proven and probable reserves at 2.9 billion barrels of oil equivalent – not 20 billion.

To reach the higher figure requires adding contingent and highly uncertain prospective resources, volumes that might never be commercially viable for production.

The North Sea basin is “mature”, most accessible oil and gas has already been extracted, and production has been naturally declining for 25 years. The vast majority of future production is expected to come from fields already producing or being developed. Further licensing will not reverse this natural decline – and the data on new licences awarded in the last decade shows it has only made an “incremental difference” to overall production.

Even Offshore Energies UK’s (OEUK) own 2025 forecast concedes the point. It projected a 3% rise in production in 2025. After 2026, production is expected to enter a natural decline so steep that the widening gap between production and demand cannot be closed by new North Sea licensing.

A Marginal Upside at Best

The NSTA does say there is an opportunity to restore output from around 200 shut-in wells, with a production potential of approximately 20 million barrels of oil equivalent. With the basin producing around one million barrels a day, that volume represents roughly 20 days of output.

However, that’s a drop in the ocean that would do little for British energy demand. Britain’s total annual energy consumption is the equivalent of about 1.2 to 1.3 billion barrels of oil, which means this could squeeze out about 1.5-1.7% of that.

The flagship field most often invoked is Rosebank. But strip away the industry-friendly framing and Rosebank’s national significance shrinks rapidly.

Equinor and Ithaca say the field contains around 300 million barrels of oil equivalent, with a lifespan of roughly 25 years. The industry often cites maximum figures of what can be produced from the get-go. This is misleading as fields tend to start high but degrade over time, producing less and less. A more accurate approach is to look at the average output over the lifetime of the field, which would be about 12 million barrels of oil equivalent a year, or roughly 32,900 barrels a day.

Given that Britain’s total primary energy consumption last year was about 1.2 billion barrels of oil equivalent, Rosebank would meet only about 1% of Britain’s total annual energy requirement on average over its producing life. Not quite the bonanza exclaimed by the fossil fuel lobby and its amplifiers.

ENJOYING THIS ARTICLE? HELP US TO PRODUCE MORE

Receive the monthly Byline Times newspaper and help to support fearless, independent journalism that breaks stories, shapes the agenda and holds power to account.

We’re not funded by a billionaire oligarch or an offshore hedge-fund. We rely on our readers to fund our journalism. If you like what we do, please subscribe.

The Hidden Problem: A Shrinking Energy Surplus

There is a deeper flaw in the “drill more” argument that rarely gets discussed. It is not only about how many barrels remain under the seabed. It is about how much usable surplus those barrels still deliver to society once the effort and cost of getting them out is accounted for.

Energy analysts measure this using a concept called Energy Return on Investment – or EROI. In simple terms, EROI asks how much energy a source yields for the energy, materials and capital put in.

A high-EROI source produces a large surplus after paying for its own extraction – surplus that supports transport, industry, hospitals, schools, households and public services. But as EROI falls, more of the economy is devoted simply to producing energy, leaving less for everything else. A mature oil basin can still produce oil barrels in gross terms – but due to declining EROI, it ends up delivering far less net energy to society and the economy.

That is the North Sea’s problem today. A peer-reviewed study of the Forties field – one of the UK’s most important oilfields – found that its net energy return fell by 46% over the period modelled, with the decline accelerating once operators had to introduce more energy-intensive support systems to keep production flowing.

A broader North Sea proxy study on Norwegian petroleum found oil-only EROI falling by 56% from 1996 to the late 2000s as depletion advanced.

The financial data tells the same story. A Parliamentary Office of Science and Technology (POST) briefing says average unit operating costs in the UK Continental Shelf (covering parts of the North Sea, North Atlantic, Irish Sea, and English Channel) rose from £13.82 per barrel of oil equivalent in 2020 to £19.49 in 2024 – an increase of more than 41% in four years.

The old era of easy North Sea abundance is over. Investing more in the North Sea is throwing money at declining returns.

Even on OEUK’s own optimistic assumptions, the extra production unlocked by looser tax and regulatory conditions the industry is demanding amounts to only about 3 billion barrels of oil equivalent spread over 24 years — roughly 125 million barrels of oil equivalent a year. That’s only 10% of current annual UK energy demand — and this is a gross figure before accounting for declining net energy returns.

Trump Went to War With Iran to ‘Seize Oil’ as US Shale Enters Major Decline

The United States launched a war on Iran, not to eliminate a nuclear threat, but to seize control of the world’s last major accessible oil reserves

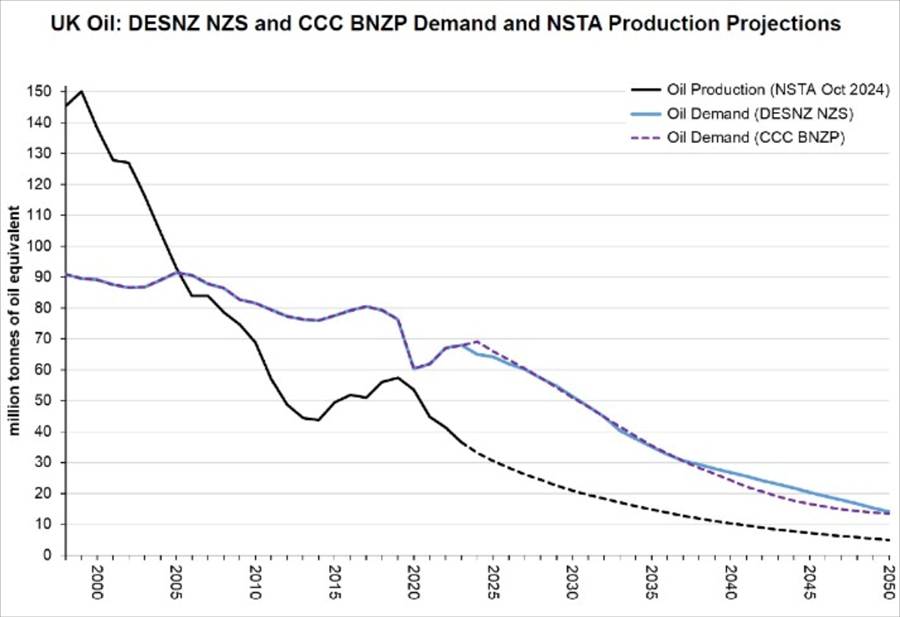

No Price Relief for Consumers

Even if every barrel arrived as hoped, it would not do what proponents imply. The tiny share of national energy demand that more North Sea drilling might be able to meet would not even be reserved for Britain.

That’s because most crude oil produced in the UK is not consumed in the UK, due to market factors and industry choices – it is processed by refineries abroad because Brent-type crude is in high demand internationally and is simply not as commercially attractive to UK refineries.

UK oil companies therefore export much of the crude produced in the North Sea and import other crudes and products that better fit refinery needs. So even if we managed to ramp up North Sea production far higher as the industry hopes, it wouldn’t actually support British energy demand – but would be exported into a globally traded system. And as the quantities are so low, it would not alleviate rocketing globally-determined oil prices.

Even when you can actually consume domestic production, that still has no impact on bills. In 2022, although nearly half of UK gross gas supply came from the UK Continental Shelf, that did not protect households from the energy price shock – the price cap rose by more than £2,800 in a single year for a typical household.

So even if we did ramp up drilling in the North Sea, what the oil lobby is not admitting is that British households and businesses would still pay prices. Who really benefits, then, from this marginal extra output? Not British consumers, but the oil industry producers selling into the international market, eager to maximise profits while the prices is going up and up.

The Public Bill

And when the drilling stops, the public pays again. The NSTA forecasts £44 billion in decommissioning costs across the basin, with £27 billion due by 2032. HMRC says the associated tax repayments and lost revenue amount to £11.7 billion — money that comes, one way or another, from the same taxpayers being told that more drilling will protect them from high energy prices.

The lobby argument is that Britain can drill its way to cheaper, more secure energy. The industry’s own evidence says it cannot. Operating costs have risen 41% in four years. The basin’s average net return has turned negative. Consumers got no price relief in 2022 even when nearly half of UK gas came from domestic fields — and they would get none next time either. Neither would British industry, which become locked into chronically high fossil fuel bills.

By contrast, a serious clean-energy buildout could cut Britain’s dependence on oil and gas far faster, and at far greater scale, than more North Sea drilling ever could. A mostly clean electricity system is achievable within five years through a crash expansion of wind, solar, batteries and grid infrastructure. And because electricity is the foundation for electrifying transport, heating and industry, that opens the way to cutting much broader fossil-fuel dependence across the 2030s, while fast-tracking Britain into the next generation of high tech energy innovation.

The extra North Sea output industry says could be unlocked by friendlier tax and regulation amounts to only about 10% of current annual UK energy demand on a gross basis, still sold into globally priced markets.

A clean-power-and-electrification strategy, by contrast, is not a marginal addition to the old system. It is the beginning of a different system altogether — one capable of breaking Britain’s structural exposure to oil and gas shocks rather than merely slowing their decline.